The background

Care organisations and many charities work directly with vulnerable adults and children. That work is essential — and it carries an unavoidable safeguarding exposure.

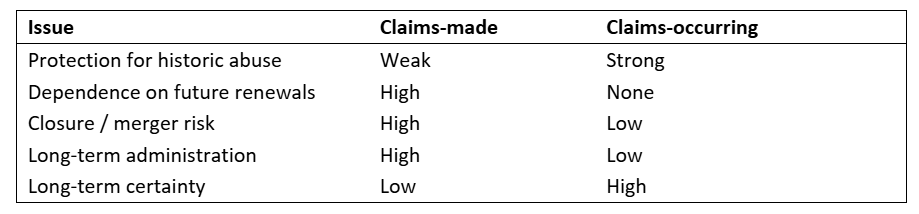

Even where organisations have strong policies, rigorous recruitment, and well-embedded safeguarding practices, the risk of abuse can never be reduced to zero. When allegations arise, the consequences are profound: for individuals, for organisations, and for those responsible for governance.

Safeguarding insurance exists to protect organisations when the worst happens. But because abuse claims often emerge many years after the events in question, the way that cover is structured matters just as much as whether it exists at all.

Abuse may only be disclosed later in life, following therapeutic support, regulatory investigations, public inquiries or changes in personal circumstances. Recent legal developments — including the removal of the three-year limitation period for child sexual abuse claims following the Independent Inquiry into Child Sexual Abuse (IICSA) — have extended the potential exposure even further. Courts also retain discretion to set aside limitation in certain adult abuse cases.

The practical consequence is clear: safeguarding cover must be considered not only in the context of today’s operations, but in relation to historic activity and the decades to come.

Differing insurer attitudes

As case law has expanded the scope of vicarious liability, to encompass claims made against organisations due to abuse perpetrated by employees, insurers have reassessed their appetite for safeguarding risks.

Some insurers now have no appetite for risks involving abuse exposure, making them unsuitable for much of the charity and care sector. Others are willing to provide cover — but on very different terms, and with very different implications over time.

Superficially similar policies can offer markedly different levels of protection once a claim arises. Understanding how cover is structured before it is placed is therefore critical.

Claims-made vs claims-occurring cover

Insurers providing safeguarding cover generally do so on one of two bases.

Claims-made

Protection depends on the policy being in force when the claim is made.

Under a claims-made policy, cover is triggered when a claim is first made and reported during the policy period, regardless of when the alleged abuse occurred — provided it is after any retroactive date stated in the policy.

The retroactive date is the earliest point from which abuse claims will be covered. As long as cover remains in place, the retroactive period grows with each passing year.

Claims-occurring

Protection depends on when the alleged abuse occurred — not when the claim is reported.

Under a claims-occurring policy, cover is triggered by when the abuse is alleged to have taken place. A claim made many years later is handled by the policy in force at the time of the alleged incident.

The practical implications - Information retention

Abuse is a ‘long-tail’ risk. Claims are often made decades after the alleged events.

Under a claims-occurring basis, organisations must retain clear records of historic insurance arrangements. If a claim arises, the relevant insurer will be the one providing cover at the time of the alleged incident.

Claims-made cover can appear administratively simpler, because claims are handled under the policy in force at the time they are made. However, this simplicity masks additional complexity. Where multiple allegations relate to the same alleged perpetrator, insurers may treat them as a single claim – meaning the first insurer on risk becomes critical, and accurate historic records remain essential.

Reliance on continuous cover

Claims-occurring cover provides certainty once purchased. If cover later lapses — for example following a restructuring, merger or cessation of operations — historic protection remains intact.

Claims-made cover operates very differently. For cover to respond, a policy must be in force at the time the claim is made. If cover lapses for any reason, historic protection may be lost entirely.

This creates particular risk where organisations undergo change. Even after operations cease or a business is sold, safeguarding exposure can remain open-ended. Run-off options may be expensive, limited, or unavailable — particularly given the removal of limitation periods.

Market appetite

Claims-made cover also assumes that insurers will remain willing to provide safeguarding protection indefinitely.

If an insurer withdraws from the care or charity sector, an organisation may need a replacement insurer to accept a long retroactive period — often in difficult market conditions, and especially challenging where claims have already arisen. Cover that has been paid for over many years is therefore not guaranteed to continue.

Claims-occurring cover avoids this dependency. Once cover is in place for a given period, it cannot be withdrawn retrospectively. While future placement could still present challenges, historic protection remains secure.

Cost considerations

Initial premiums for claims-made and claims-occurring cover are often similar. Differences emerge once claims arise.

Under claims-occurring cover, claims typically attach to historic policy years, often with a different insurer to the one providing current cover. This limits the impact on present-day premiums and allows pricing discussions to focus on current safeguarding practices, which are often more robust than those in place historically.

Under claims-made cover, claims relating to historic abuse can affect the current insurer directly. This can lead to sharp premium increases and reduced market options. Replacement insurers may scrutinise historic safeguarding practices closely when asked to accept a retroactive period that includes known losses.

Summary comparison

Other considerations: limits of indemnity

Beyond the basis of cover, it is essential to understand how policy limits apply.

A small minority of insurers provide safeguarding cover on a “silent” basis within the full public liability limit. Most, however, impose an aggregate limit for all abuse claims — either per policy year (claims-made) or per period in which abuse is alleged to have occurred (claims-occurring).

In either case, limits must reflect the potential for multiple claims to erode a single limit, particularly where allegations relate to the same alleged perpetrator.

Under claims-occurring cover, limits should be as future-proof as possible. A policy purchased today may be relied upon many years from now, when settlement values may be significantly higher due to inflation and changing legal attitudes.

Claims-made cover theoretically allows limits to be adjusted at each renewal. However, this assumes continued insurer appetite. Insurers may reduce limits at the very point an organisation is seeking increases to keep pace with inflation. In addition, earlier policy years may still apply if claims are linked.